A few years back, I was brought in by the president of a small business which manufactured and installed custom storage systems for offices and restaurants. His concern was that either his accounting system had a bug in it or that someone was stealing from him.

This came to light when he ran his most recent quarter profit and loss; it seems that for the first time in over 7 years, he lost money. His shop has never been busier. He is getting lots of highly profitable contracts so the quarterly results don’t make any sense. I asked to see quarterly information and got to work.

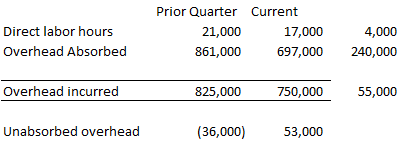

The first report I reviewed was the profit and loss report. Sure enough, there was a $53K unabsorbed overhead amount This happens in one of two ways – quarterly overhead went through the roof or the driver, in this case direct labor hours, were substantially lower. Sure enough, the direct labor hours were down about 10%, indicating that labor wasn’t recorded. Which would be really strange as the controller had been doing this job for almost 5 years and consistently made the overhead allocation adjustment correctly.

So I asked the president if there were any major changes. His response was that he decided to outsource all of his installations. As a test, he explained, the company in the prior quarter elected to put the installation out to bid on one project and the price came in at about 60% of what his costs were. So he decided that he was going to “sell” the installation department to his department supervisor who would then quote jobs as an independent contractor.

I explained to him that what he was seeing was a direct result of the decision to outsource without knowing all the available facts.

Fact: There were two different departments, each with its own overhead costs and driver

Fact: the Company was using a single driver addressing the total overhead

Conclusion: The same (essentially) overhead dollars were being allocated over fewer direct labor hours, leading to larger unabsorbed overhead since the rate was not adjusted to reflect that fewer hours were being “sold”.

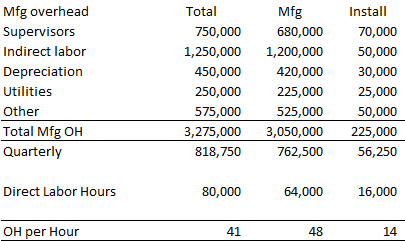

I then showed him a spreadsheet of what this actually looked like:

The company rate of $41 was correct, but only for its overall purpose, allocating company overhead to production costs. In reality, very little of the overhead went to support the installation department. As a matter of fact, when separated, it became obvious to him that the shop was being subsidized by the installation department.

When they bid a job and included the rate of $41 to the install hours, the company was in fact generating an additional $27 in revenue which went to the bottom line. But this was hidden from the controller, the president and the estimating department. Thus, the $100 per hour revenue rate appeared high when compared to the $75 rate that the subcontractor offered.

In truth, had the company been facing lost estimates, they could have reduced the hourly rate for installations from $100 to about $65 and still earned a decent profit. But you have to look deeper into your company structure in order to understand that options like that are available to you.

When most of your costs are fixed, then basing make or buy decisions on your overhead absorption rate can be dangerous. The key is understanding that allocating costs by way of hours turns that fixed cost into an illusory variable cost. You begin to think that by eliminating the driver, the cost goes away as well. It doesn’t work.

Once the president understood this, he was able to convince the installation team to rejoin the company, although he did have to make some concessions as to bonuses when it came to profit earned on installation jobs. And with this information, the company went through the various areas of the business and examined how costs were incurred and allocated to projects to even more effectively estimate contracts and keep their bids competitive while improving their profitability.