Accounting is a universally accepted lagging indicator. Profits are so last month, the balance sheet is yesterday’s news, and don’t get me started on net book value of equipment. As strange as it sounds though, most people making decisions seem to be ok with all the things that happened yesterday and in some cases things that happened years ago.

One of my favorite lines in a presentation is, “Running your business by your accounting information is like driving with your windshield blacked out and being forced to steer by looking in the rearview mirror.” It is dangerous and will ultimately run you off the road and yet many people find comfort in looking at past performance and remembering the good old days. But you have to start looking at other things in order to make better decisions.

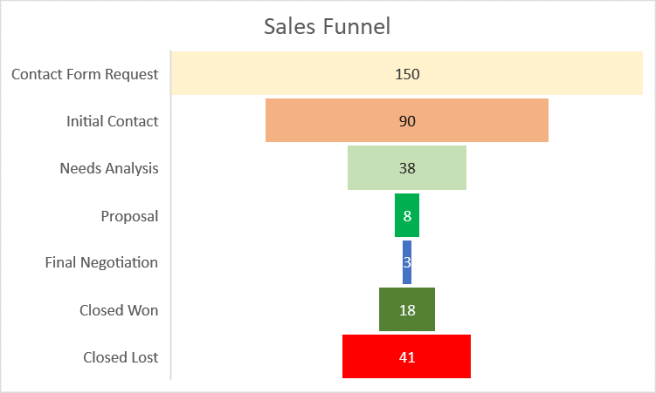

Let’s start with revenues. Quick question, are you tracking your sales funnel?

Looking at this, we can begin to make an educated guess at where sales are heading next month and perhaps beyond. With $30K sales in final negotiations and $80K in the proposal stage, you know that with a closing ratio of about 45%, you are looking at close to $50K in revenues closing in the next month. Meaningful? Compared to saying that the company did $42K last month and $68K in the same month last year?

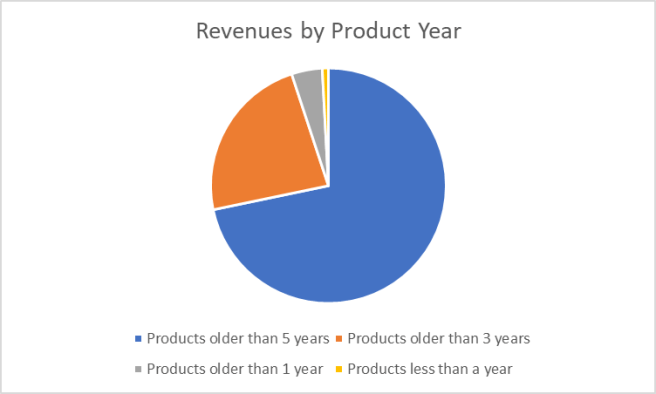

While it might not seem like a leading indicator, this one could be if properly used. This tracks the revenue by products, not based upon their model, but based upon the year that it was originally introduced. If your company prides itself on bringing new products to market but you are unsure how new products fare, this could be an eye opener. In this particular case, the bulk of the revenues is generated by legacy products, followed closely by near-legacy product sales. Is this a problem? Perhaps, especially if you find out that your advertising and promotional dollars are being spent to keep legacy products in front of customers, or that you are spending a ton of money on advertising the new hotness and it is not taking off.

This reminds me of a recent conversation I had with a client. It seems that one of their major customers is going to merge and most likely will no longer buy products from them. The obvious question, how are you going to address the concern?

No problem he says. They are going to lay off employees. We have been spending almost $750K a year on R&D and we haven’t gotten anything out of it.

I was voting on cutting senior management compensation by 98% and moving them to some sort of incentives based on new products and new channel sales but I guess slowly going bankrupt by starving the company of new products is a much safer bet. After all, every “VP” should be guaranteed a paycheck.

Find a creative way to look at your company’s data, especially sales. If you are not tracking sales prospects, start now. Your sales people will give you lots of reasons why it won’t help, but don’t take no for an answer. If you have new products that are not selling, find out why. My bet is that somewhere along the way there is a disincentive to either buy or sell. Customers are getting a better deal on your old products or your sales peoples’ commissions are better on legacy products. Or it is a dog and you need to dump it!

Don’t simply rely upon accounting reports when it comes to managing your business. Get creative, tell your controller or CFO to get creative when it comes to predicting future sales and expenses. Yesterday’s news is important to someone, but that someone doesn’t have to be you.